We’re raising the financial IQ of the world

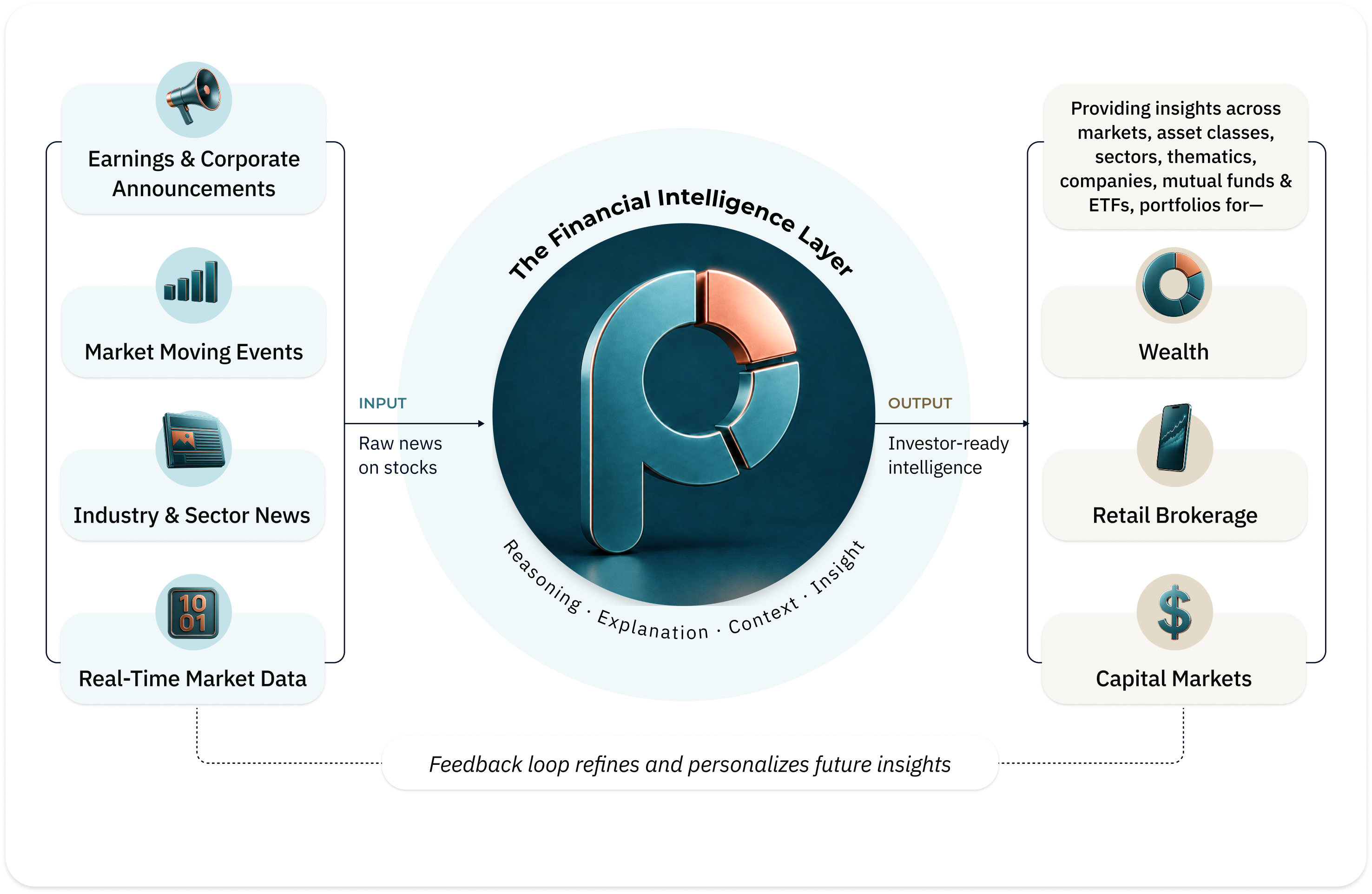

We believe financial understanding should be universal. That technology shouldn’t simply make markets faster, it should make them more understandable. Here’s how we achieve our vision.

Democratize understanding

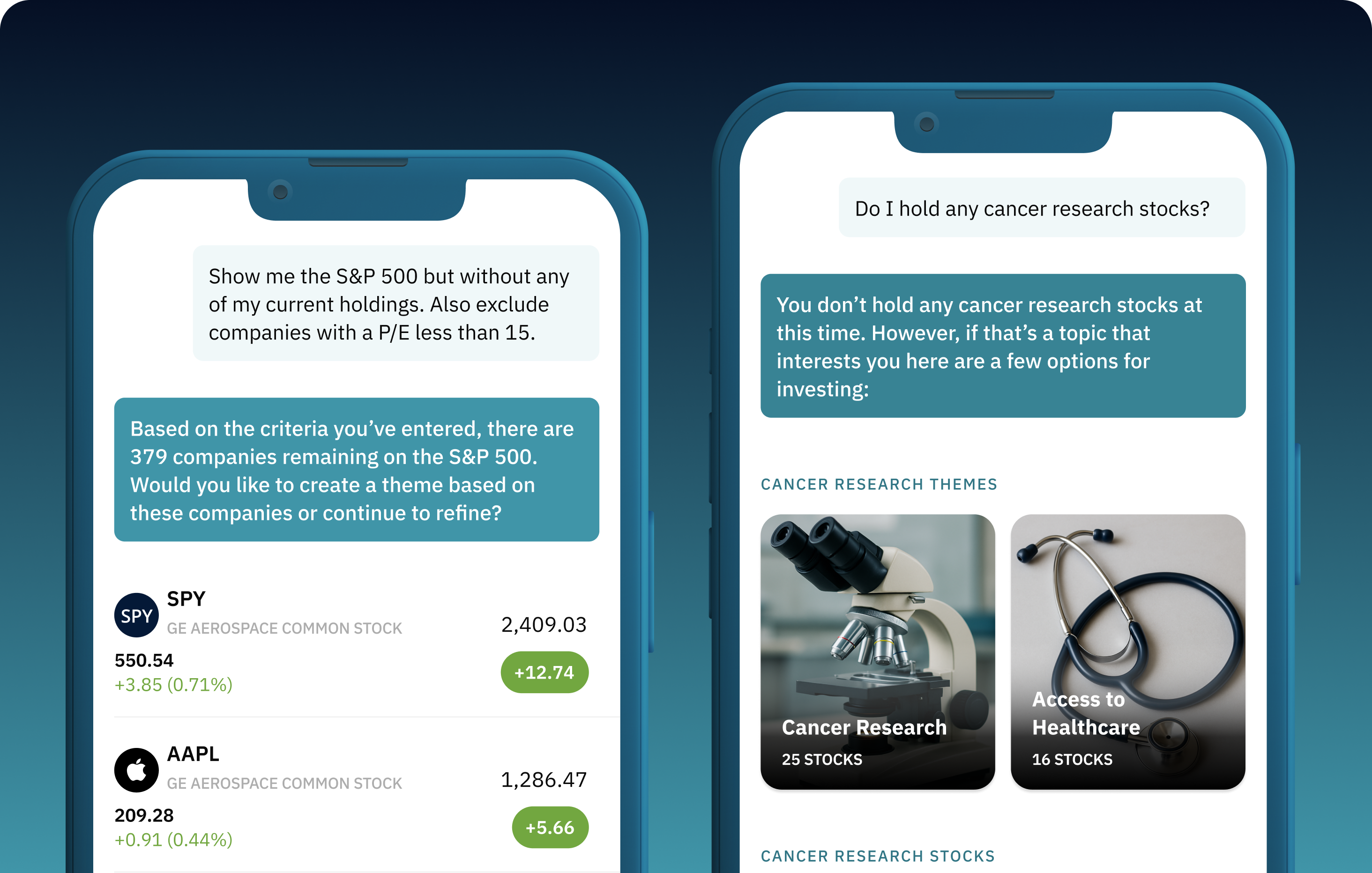

More information used to mean less understanding. With Pebble, you can have both.

Reduce complexity

We transform thousands of market signals into one coherent, succinct story, without the financial jargon.

Augment, don’t replace

Our goal is to empower investors (not replace them), so more informed decisions can be made, faster.

Trust and verify

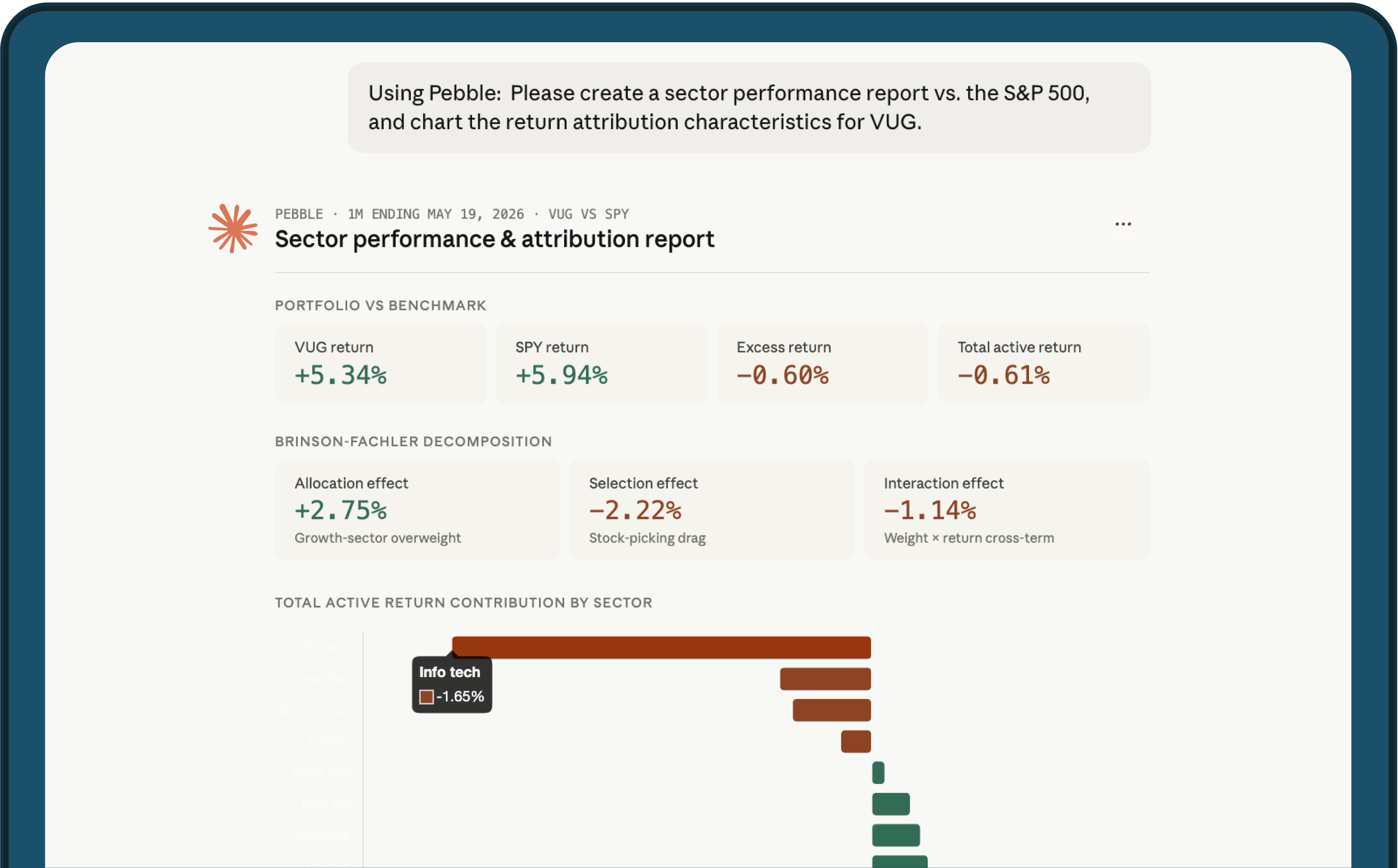

To become trustworthy, we believe financial AI must be explainable, attributable and compliant.

Pebble delivers fiduciary-grade AI directly to your investment workflows.

Get instant, clear insights powered by real-time data with advanced AI that’s purpose-built for finance.

We aren’t another platform, LLM or GPT wrapper.

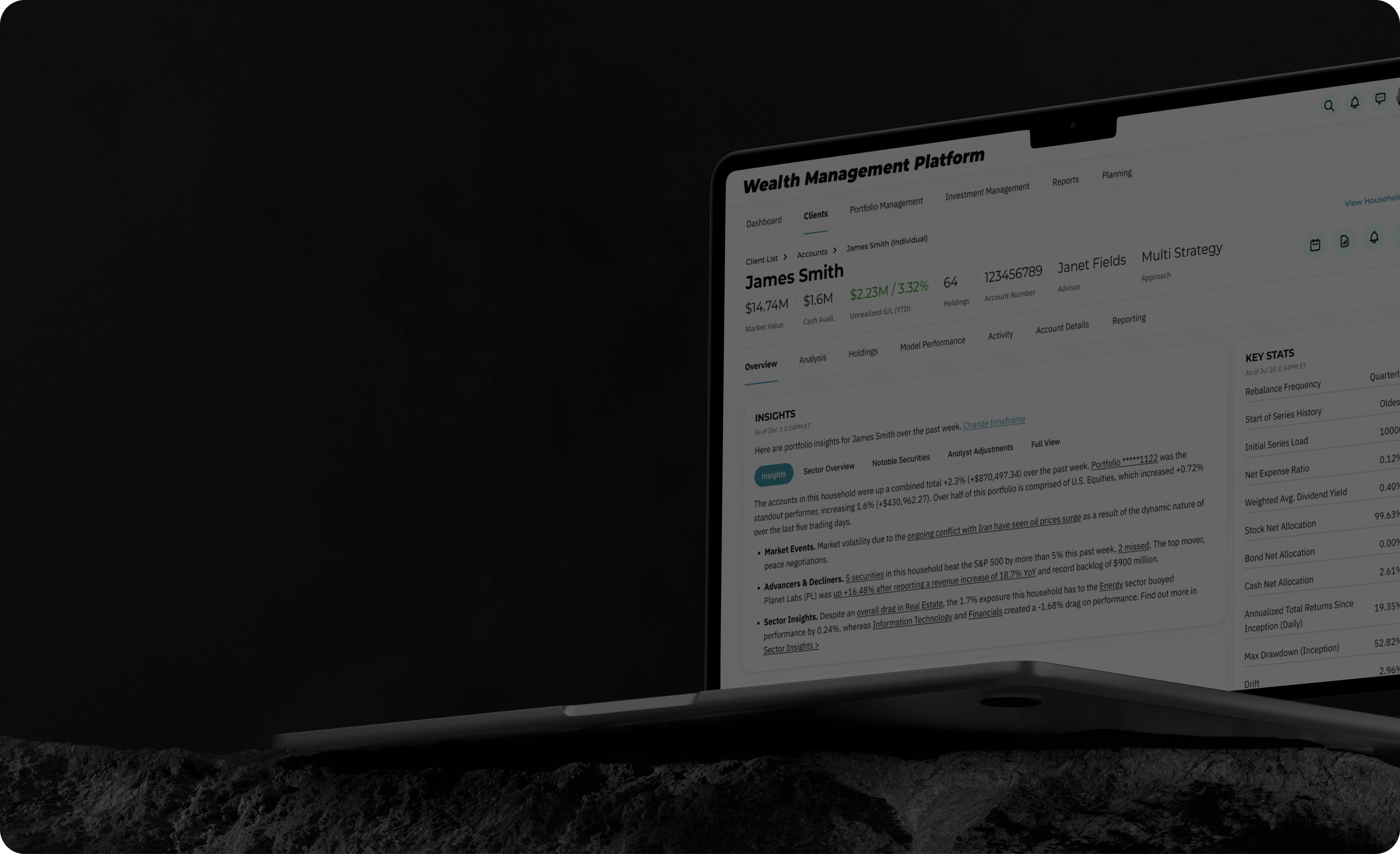

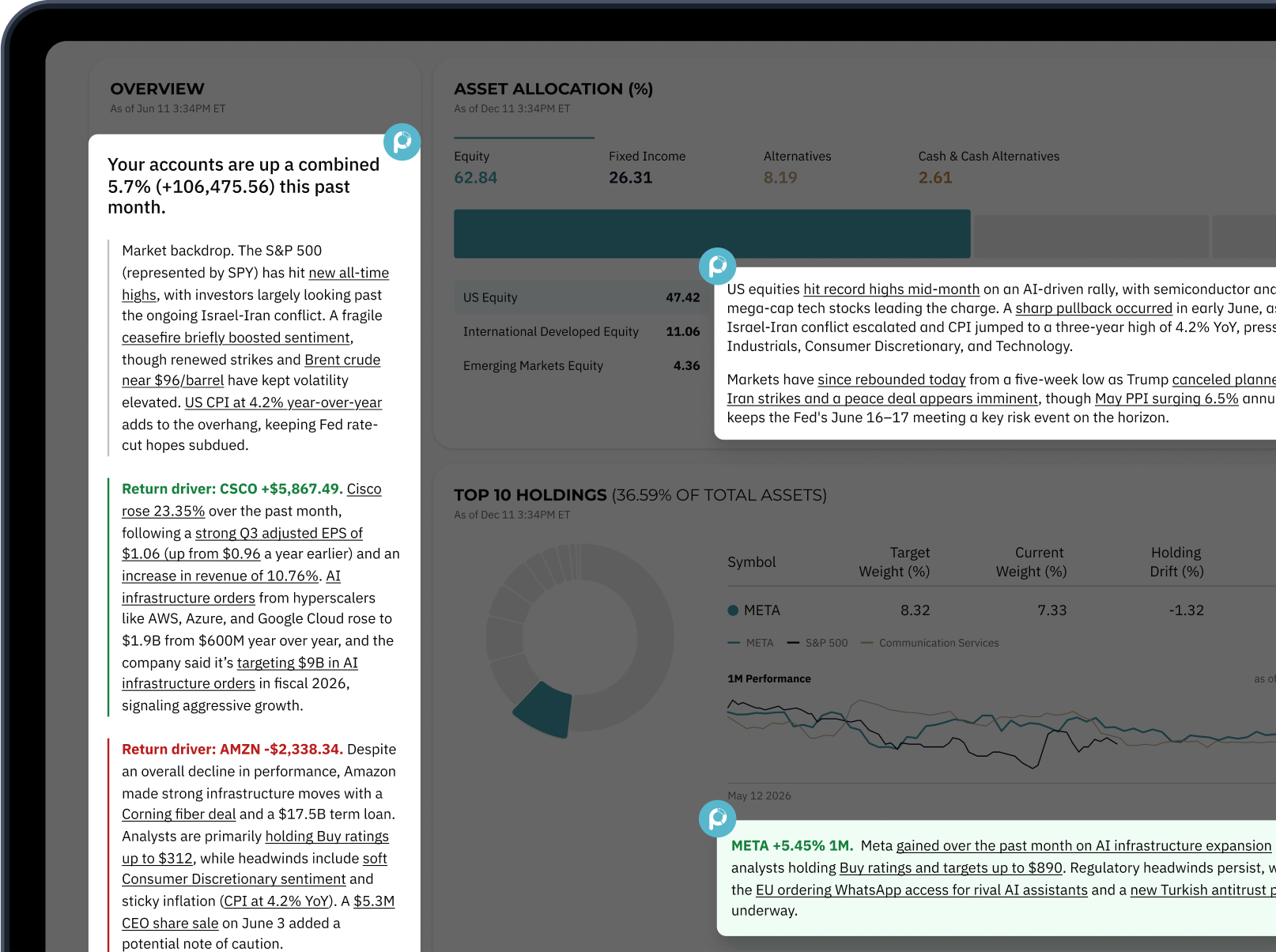

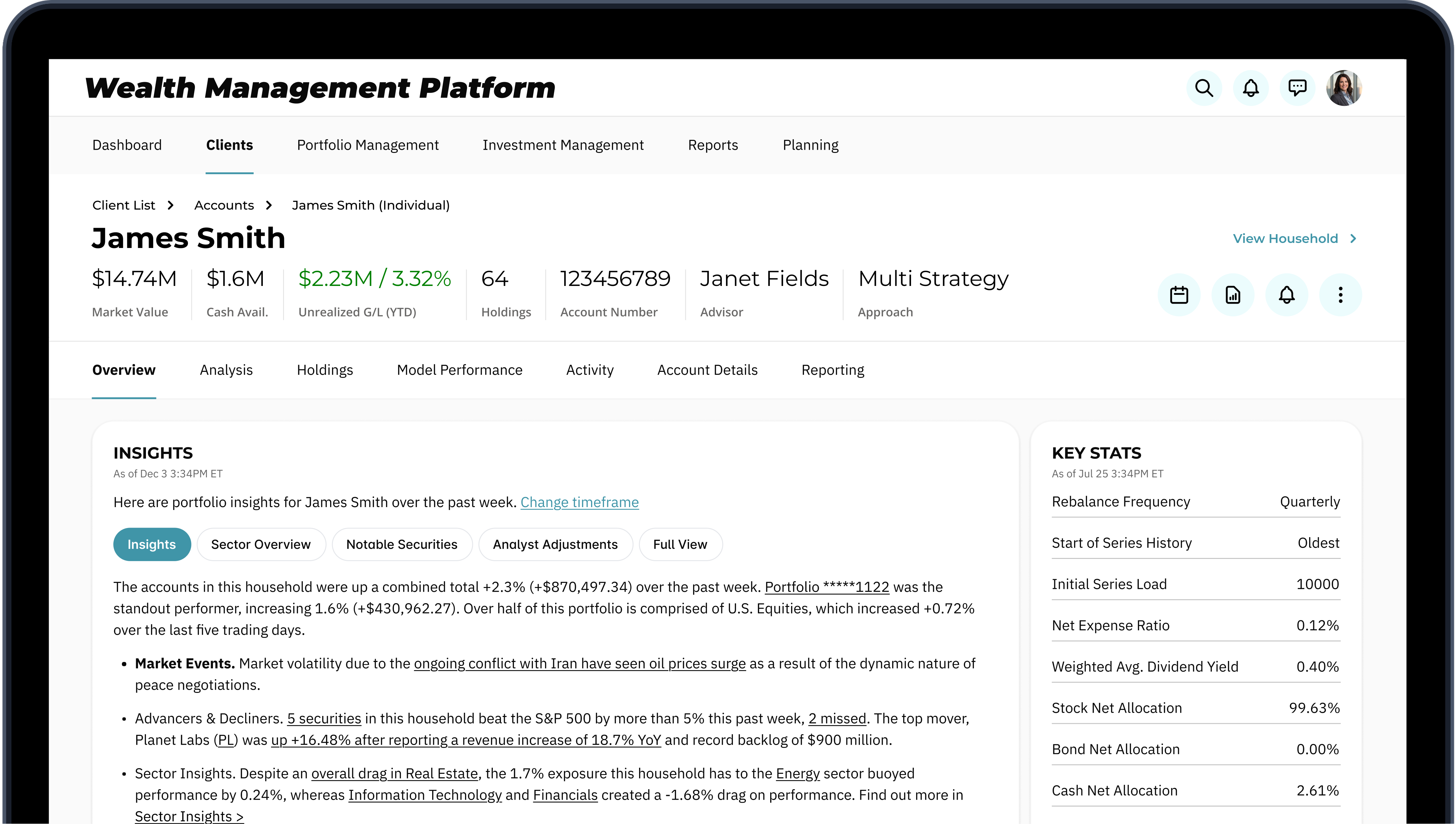

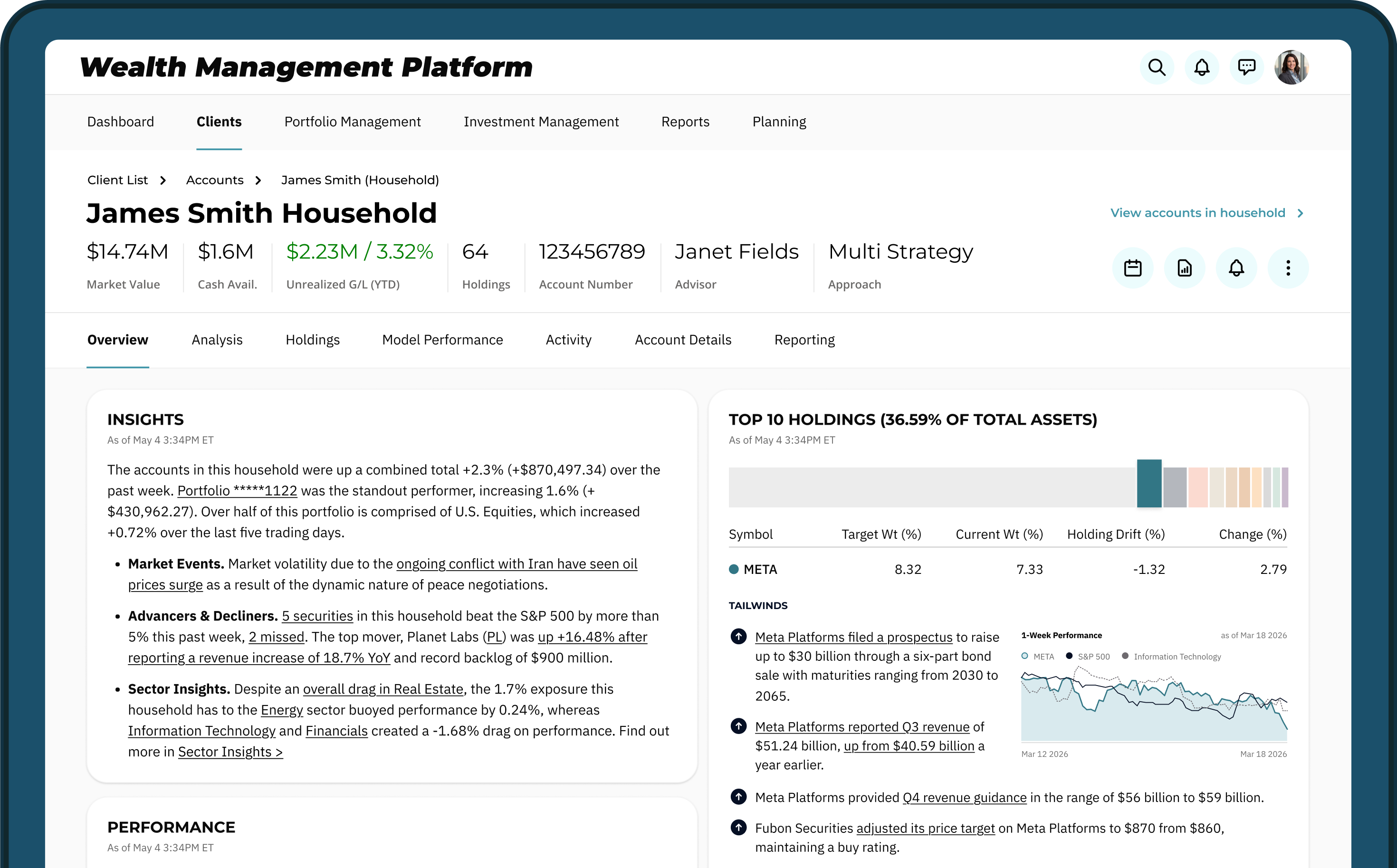

Pebble helps wealth and investment firms deliver the why behind performance by embedding AI-powered market and portfolio intelligence directly into their platforms, enhancing advisor, client and analyst workflows.

The result? Stronger engagement, greater productivity, compounding time savings and accelerated AUM growth.

Who we serve

We deliver purpose-built intelligence for organizations that are shaping the future of investing. Pebble's AI is tailored to each firm in order to meet rapidly evolving client expectations.

Wealth Management

Increase client service quality and advisor productivity without increasing headcount through AI-powered portfolio and market intelligence.

- Automated client review preparation

- Personalized portfolio commentary

- Risk, exposure & performance explainability

- Advisor copilots for client engagement

Retail Brokerage

Drive investor engagement with AI-powered market and portfolio intelligence that increases activity, retention and asset growth.

- Personalized investor insights & explainability

- AI-generated alerts, commentary & watchlist intelligence

- Copilots for education, discovery & trading

- Portfolio reviews at scale

Asset Management

Strengthen investor communication and accelerate distribution with scalable AI-generated portfolio intelligence and fund commentary.

- Automated fund and portfolio commentary

- PM and sales intelligence copilots

- Risk and exposure explainability

- Investor reporting automation

Information Providers

Unlock new AI-native distribution channels by transforming financial content into interactive, explainable and conversational investment intelligence.

- AI-native news & research experiences

- Conversational delivery across wealth platforms

- Embedded market and portfolio explainability

- Personalized insight and commentary generation

The hard part isn't building AI. It's scaling it

Financial institutions are discovering that AI prototypes built on generalized LLMs become costly, unpredictable and difficult to govern at scale. Pebble was purpose-built for the operational realities of enterprise AI in regulated finance.

AI economics at scale

What works in a prototype often breaks under enterprise usage. With Pebble you can:

- Eliminate runaway token & inference costs

- Deliver sub-second insights across millions of portfolios

- Build for predictable enterprise-scale operations

Built for compliance from day one

Regulated firms need more than powerful models. Luckily, Pebble has:

- Human review & approval workflows built in

- Explainable outputs designed for oversight teams

- The structure for evolving regulatory expectations

From AI strategy to production

Most internal AI initiatives stall long before enterprise deployment. Pebble helps you:

- Avoid multi-quarter infrastructure rebuilds

- Deploy enterprise-ready capabilities immediately

- Accelerate time-to-market without expanding engineering teams

Connection-ready insights delivered in days, not months

Pebble is optimized for rapid implementation. Collaborate directly with our team to get up and running in days.

Simple authentication

API key authentication: get API key → call service → done

Simple REST API

All APIs are versioned, stateless REST APIs with full documentation

Simple JSON data models

- All payloads, both request & response, are JSON data

- Inline markdown is used for URLs

- URLs can be customized via templates

Interactive API response times

- Event-based architecture & extensive caching allow us to offer sub-second response times with real-time data

- No more waiting seconds for an LLM to process a request!

No user PII needed

All API calls are ephemeral & anonymous

Robust QA

- All results are evaluated for factual accuracy

- SLA guarantees for factual accuracy (95%+)

- No more hallucinations or logical fallacies

- All facts are source-cited to the original content

Fully customizable

- Data is returned in "raw" format, leaving you full control over formatting & branding

- No iframes, HTML, or pre-formatted content to deal with

- Content is free of Pebble branding, allowing you to integrate directly into your application

Rapid deployment

Existing clients have gone from idea to production in ~30 days

We have the first regulator-blessed AI built for finance

Our team has over 100 years of combined experience working with complex, critical and sensitive financial data. We're working to set the industry standard for compliant Financial AI, delivering commentary built to align with regulatory guidelines for accuracy, bias and governance.

This means your data is safeguarded under rigorous, independently-verified security controls that meet industry-leading standards.

Over 99% accuracy rate

Over 99% accuracy rate

Accuracy checks & constant evals

Accuracy checks & constant evals

Human in the loop reviews

Human in the loop reviews

Zero client data retention

Zero client data retention

Secure enterprise cloud

Secure enterprise cloud

On-premises option available

On-premises option available

Discover the Pebble difference.

Find out how we can work together to help your people make smarter, faster investment decisions with financial AI.

Check out the latest resources from Pebble

Fintech's Control Is Slipping As Advisors Start Building Their Own Solutions

Generative and agentic AI are turning financial advisors from users of technology into builders of it — and that shift is redrawing the relationship between advisors, fintech firms, and the clients they serve.

Why Pebble Finance Could Change How Advisors Explain Portfolios

At Future Proof Citywide in Miami, Justin Whitehead framed Pebble around a simple idea: investing tools should make markets easier to understand, not harder to navigate.

For Now, AI Is Making Financial Advisors More Productive. What Comes Next Could Be More Disruptive

Thousands of financial advisors at the Future Proof conference in Miami last week got a glimpse of how AI is changing their industry. Here’s what they saw.

Common questions

Everything you need to know about Pebble. Can't find your answer? Reach out to us directly.

What is Pebble?

Pebble is an AI intelligence layer for wealth management, retail brokerage and asset management firms. Pebble transforms market events, portfolio activity and financial content into personalized investor insights, commentary and explainability experiences.

What problems does Pebble solve?

Pebble helps financial institutions scale investor communication, increase engagement and automate manual analysis workflows. Common use cases include portfolio commentary generation, market and portfolio explainability, advisor and investor copilots, investor alerts and notifications, fund commentary automation, and AI-powered research and discovery experiences.

Who uses Pebble?

Pebble is built for retail brokerages, wealth management firms, RIAs, asset managers, banks, financial data providers, and financial news and research platforms.

Does Pebble integrate with existing financial platforms?

Yes. Pebble is designed to integrate with existing wealth management, brokerage and asset management infrastructure through APIs and modular AI services.

Can Pebble use proprietary financial content?

Yes. Pebble can ingest and operationalize proprietary research, news, market data, investment commentary, analyst content and portfolio intelligence — allowing firms to create differentiated AI experiences powered by their own content and expertise.