2022 Theme: Tight Energy Markets - US LNG Finally Goes Boom

In an earlier edition of this newsletter we highlighted that the tremendously low supplies of diesel and gasoline (as well as other types of fossil fuel-based energy) meant that refineries were working overtime to keep the market supplied and, yes, reap major profits.

Our commitment to being green and curtailing investments in the fossil fuel industry has, ironically, created a bonanza for that same industry.....sigh.

In our earlier piece, we worried in general terms, that working flat out without any downtime or scheduled maintenance and hot summer temperatures raised the likelihood of an combustible accident that could lead to both a complete collapse in supply and also a prolonged outage that wouldn't be easily resolved.

In other words, all work and no rest or maintenance was raising the possibility of an actual crisis - we were and are, playing with fire.

Unfortunately, we have been proven correct. Quite literally.

Or at least we were thematically correct about the risk, just not the precise region or product. We had suggested it was diesel or gasoline but Pebble Slack and many other social media forums instead lit up when a large liquified natural gas export complex in Texas suffered a major explosion and fire last week.

You can see the actual event here:

This Freeport, TX complex is a major, major natural gas exporter, accounting for roughly 17% of US capacity or around 2 billion cubic feet a day.

The plant is both the oldest and largest LNG facility in the US and increasingly exports much of its cargo (60-70% over the last 3 months) to European customers desperate to replace diminished Russian supply.

The dramatic accident has, unsurprisingly, caused some natural gas prices to soar, especially those traded or sold in Europe.

Problematically, what was initially billed as a three week blip has now become an extended pause through perhaps the end of the year.

As of the time of writing, the plan is that the plant will be completely shuttered for at least three months and will not be completely re-opened until late this year. Three short weeks has become six months.....

We raised this regrettable incident for two reasons:

Our fears about the possibility of major disruptions are not just proving correct but are also still outstanding. What has occurred in Texas with natural gas today could occur in New Jersey or California with diesel or gasoline tomorrow.

And it also provides a very interesting case study in how the global energy market reacts to an unplanned outage in an era of super tight supply.

The obvious and boring conclusion: Markets do not deal with these issues well.

More interesting however, is another of our energy themes and that is the fact that the collateral damage is also very uneven.

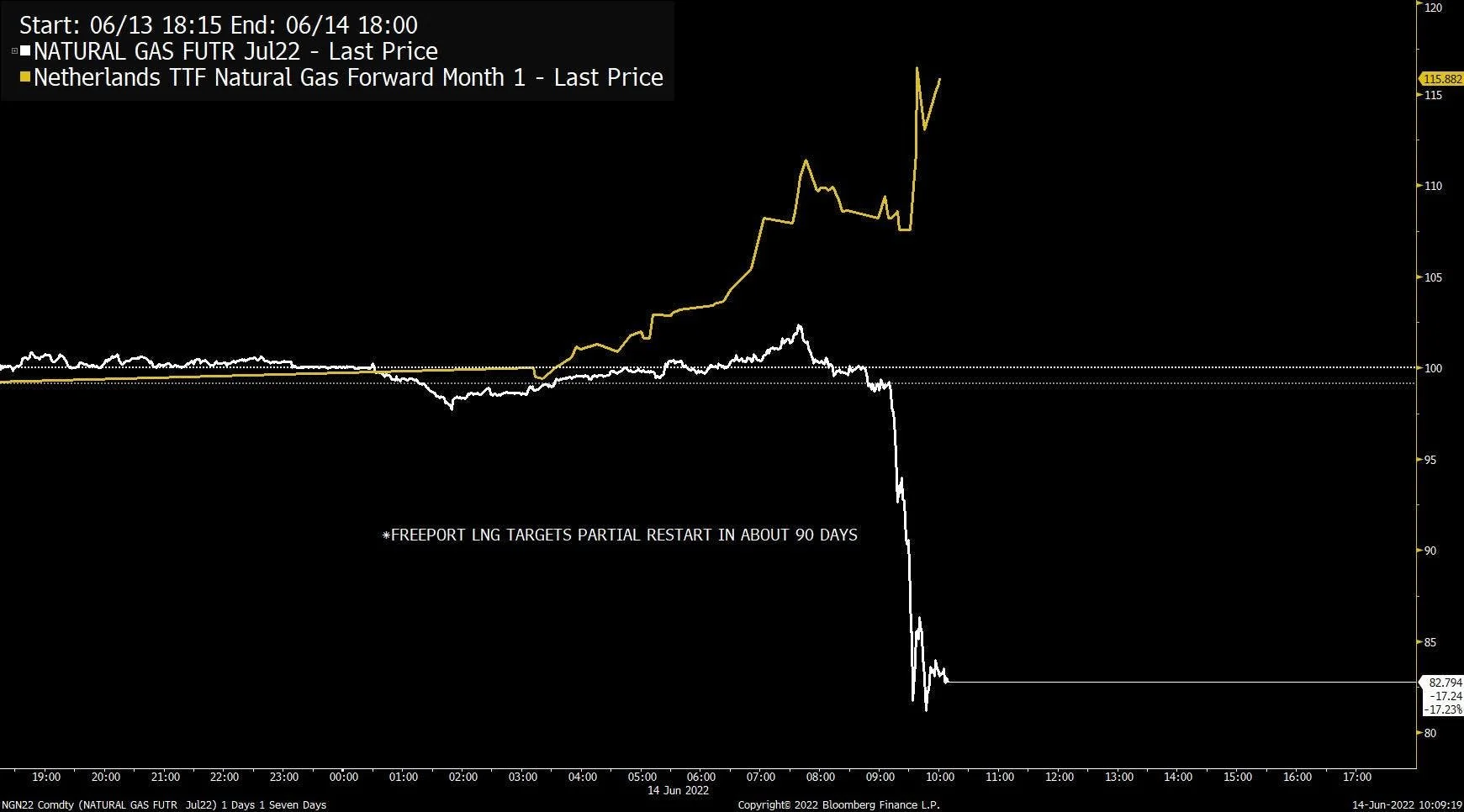

The best expression of this is that European natural gas prices rose quickly in the aftermath of the explosion and did so again after the updated announcement while, perhaps counterintuitively, US natural gas prices fell equally sharply.

Why?

Well, because the key aspect of the Freeport LNG facility is that it is an export facility - one of only seven.

And the US has obviously been busy exporting as much natural gas as possible to Europe; both to keep the lights on AND to take advantage of the far higher prices found on the European commodity exchanges.

And there won't be nearly as much exporting done now. As a direct result of the Freeport accident, about 30% of US natural gas will instead be forced to stay domestically.

This is a seismic shift in global LNG supply. US gas producers would love to send their gas to Europe but now will be constrained by a lack of capacity to do so.

The market reaction was very swift. Here is the moment where the updated and elongated schedule for repair was announced - US prices one way, European the other:

Why did this occur? Well, as a direct result of this fire in Texas, the US will be replenishing its depleted natural gas inventories for at least 3 months and maybe more. In turn, this will mean that there will be more unexpected supply next winter when US the typically draws down its gas storage inventory to stay heated throughout the winter.

And so Europe's pain is directly equal to USA's gain.

And the pain in Europe is not trivial. The summer is supposed to be the easier season of low(er) demand and prices. Instead, it is proving to be anything but either easy or cheap.

Russia isn't helping matters, either. In fact, they are piling the pressure of tight supply on. It is a bit of a moving target but by Friday Putin's regime had, at least "temporarily":

Slashed deliveries by 50% to Italy and Slovakia.

Cut France off entirely.

And this means that the French join Bulgaria, Finland, Poland, the Netherlands and Denmark with zero Russian supply.

Germany is increasingly very isolated.....

This double curtailment had a severe impact on European natural gas prices. Wholesale European prices rose 24% this past Wednesday and did so again strongly on Thursday and are, at the time of writing on Friday, up over 7% again. That makes it over 50% for the week which is the strongest for the commodity since Russia invaded Ukraine.

Here is the relevant chart:

Before our American readers feel too smug please remember that we are facing similar vulnerabilities, just in slightly different ways. And, sadly, ours aren't created by stupidly relying on Vladimir Putin's Russia but are instead entirely self-inflicted.

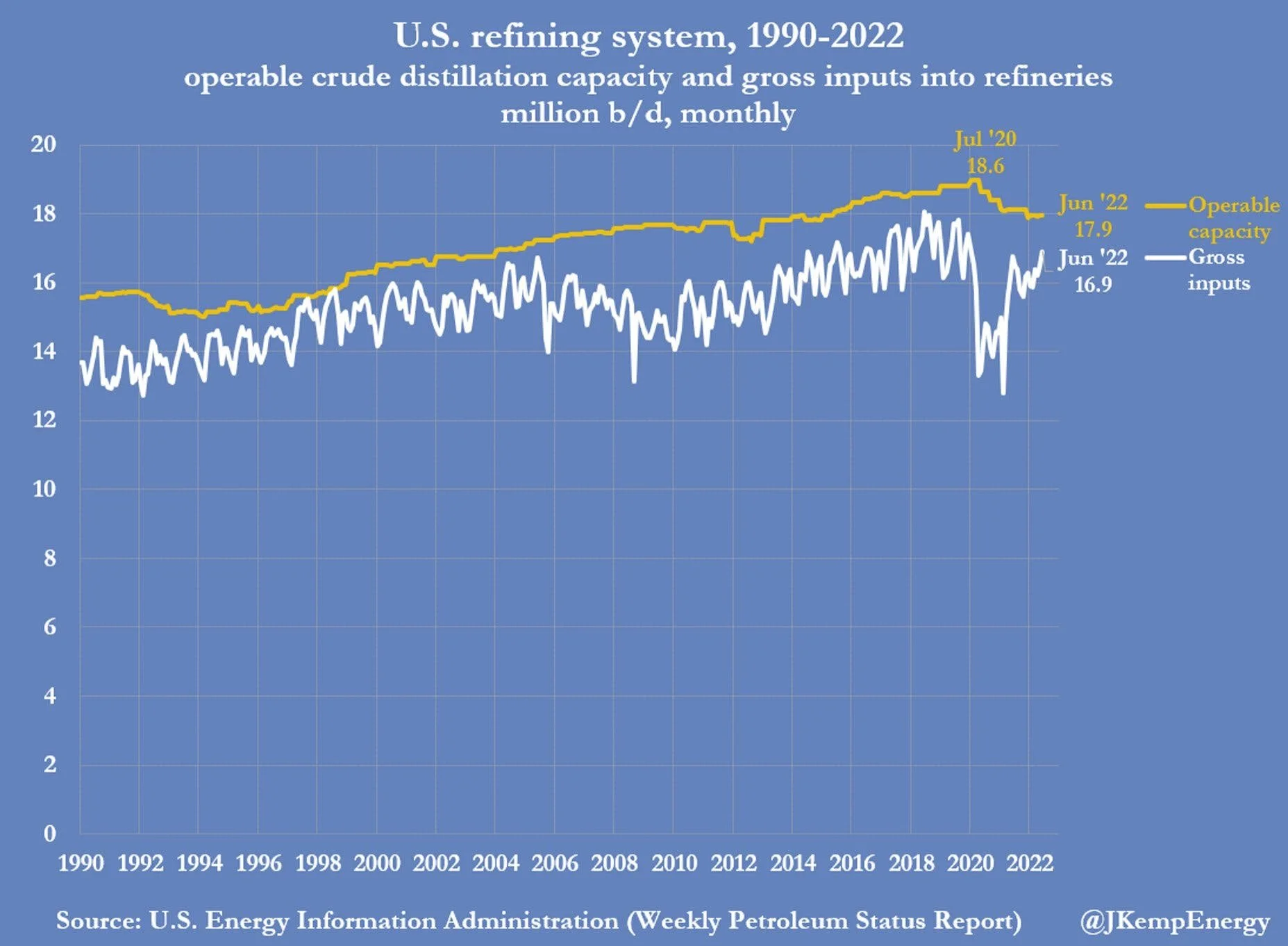

Here is the spread between how much available crude refining capacity we have compared to how much demand there is. Getting uncomfortably close.

There remains zero margin of error:

This is what nearly a decade of underinvestment in the fossil fuel industry and endless ESG blackmail has gotten us here in North America.

And what did our present Presidential administration do about this state of affairs? They wrote refiners a public letter on Thursday and suggested that they could be doing something about this situation, of course.

What should refiners do exactly? Form an illegal cartel to restrict price rises? Invent more refining capacity overnight? Go back in time and better resist the political and investor pressure to lower investment in new projects?

Even more incredible, the same President is off to Saudi Arabia to cozy up and make nice and ask for more oil supply.

Anything but encouraging investment in America's own oil and gas industry!

And if the administration simply refuses to support the US economy, then perhaps they could at least refrain from constantly alternating between either antagonizing or threatening the oil and gas industry. Fewer cheap attacks that accomplish little other than eroding trust and diminishing any hope of collaboration might be a bright start to a better tomorrow.

Let Americans have some of that political moderation, common sense and above all competence they were supposedly voting for.

*******

Have questions? Care to find out more? Feel free to reach out at contact@pebble.finance or join our Slack community to meet more like-minded individuals and see what we are talking about today. All are welcome.