2022 Theme: Inflation - Could We Possibly Flip From Inflation To Deflation In The Next Year?

It has been a few weeks since we had the pleasure of writing.....what did we miss?!

Good news it seems! Prices for all sorts of raw materials, finished goods and even services are plummeting.

Cotton, tin, lumber and plenty of other commodities, even energy and oil (though not gas or coal, sigh), have fallen steadily over the past few weeks.

It isn't just commodities either. We are seeing demand destruction for goods (things you buy) as well as services (transactions that don't involve goods).

These can be all manner of things. From haircuts to dining out to transport. The latter has been particularly affected.

For instance, here is the critical shipping rate for a 40 ft container from Shanghai to Los Angeles:

The price is down ~40% from peak and though still a looong way to go, this is real and consistent progress.

This signals not just that people are buying fewer goods - we knew that, after all, from our bullwhip work - but also that we have successfully crimped demand for commodities and this is now (slowly) flowing through into services costs.

Some of the charts are dramatic. To take just one example, here is tin:

There are plenty of others in this vein. Industrial metals are actually quietly experiencing their worst quarter since the financial crisis in 2008. Easy come, easy go.

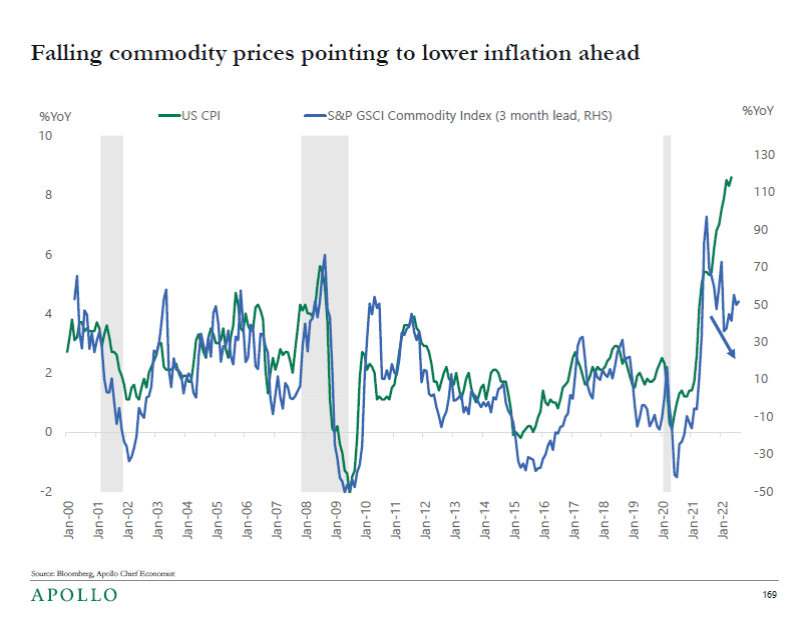

And this trend of declining prices are achieving real progress across the complex of raw materials and inputs and it should quickly begin to show up in inflation as well. Here is an index of different commodity prices versus the ever important US CPI:

It obviously suggests that, very quickly, CPI could also begin to come down appreciably. We obviously hope so.

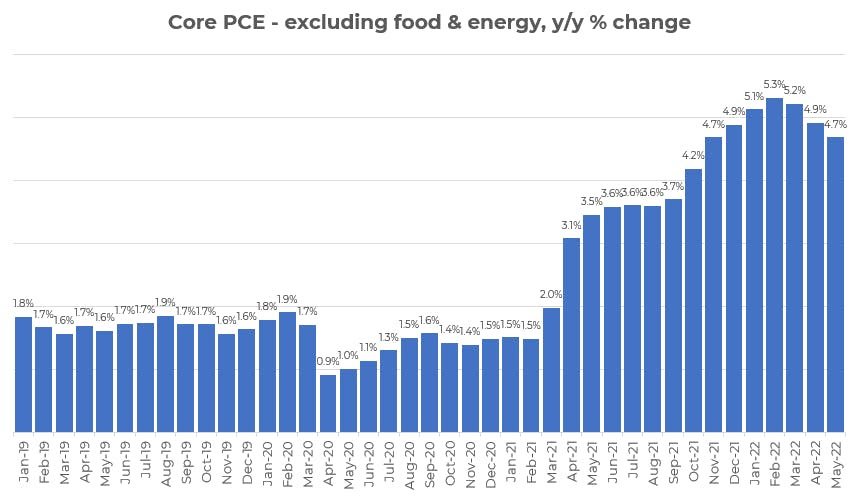

We didn't get any info on CPI this week but we did find some other US inflation data this week. The Personal Consumption Expenditure index is put out by the Commerce Department and is actually the Fed's preferred measure. It gets pretty academic as to why and you can read more about it here but essentially, PCE is less volatile than the CPI.

And there was good news here as well. Core PCE (so minus volatile food and energy) decelerated for the third straight month. It is still very high (4.7%) but it came in below expectations and the trend overall is very good, see here:

It might not look like it but this is progress. Once again, there is no guarantee it continues and there is a great distance to go before it reaches 2%.

Nonetheless, all of this adds further strength to our rather tepid call in May that core inflation might have peaked this spring and we could actually now be at risk of overreacting against it at the exact time it is decelerating.

This is a real risk because, as we have emphasized time and time again, the difficulty for the Federal Reserve is to gently slow the economy without causing it to crack and tip into a recession and its close relative, deflation.

One of the new questions is just how quickly the Federal Reserve should continue to tighten policy and rates. Now that they have finally begun to take inflation seriously, they have begun to win the war.

But that was actually the easy part. Now comes the difficult one and one that will likely require tremendously sage judgment. After the last year it is difficult to feel very confident and as Jay Powell admitted in an interview this week, even our central bank apparently doesn't know very much about inflation.

I guess that was honest but it was not exactly inspiring!

Like really everyone else we are unsure about how far or how fast prices will fall. We are more certain that the Federal Reserve will be watching very closely but how they decide what to do will be very difficult.

The odds of a Federal Reserve monetary policy mistake are not just high, if such a mistake were to occur, it is approaching in terms of time. Knowledge of that will keep markets volatile and any recoveries muted.

That isn't the only risk either. As ever with the US or any economy, there are other policies and forces that are both complicating the picture and potentially causing havoc at the exact same time the central bank is trying to glide in for the aforementioned and infamous "soft landing."

Let us explore some of the most serious examples.

*******

Have questions? Care to find out more? Feel free to reach out at contact@pebble.finance or join our Slack community to meet more like-minded individuals and see what we are talking about today. All are welcome.