The Paradigm Shifts: The Federal Reserve Raises Rates & Yet The Market Rallies, Why?

Even by the standards of an action filled year, the financial calendar was jam packed this past week.

The last 5 weekdays had:

Many of the biggest and most strategically important companies reported their earnings throughout the week.

A standard July two day Federal Reserve meeting with an interest rate increase (0.75%) on Tuesday and Wednesday.

The second quarter of US Growth Domestic Product was reported on Thursday.

The results were quite something. A short summary might be: many important companies' earnings strongly disappointed, the US central bank hiked rates by yet another 0.75% and the US officially entered a recession by recording its second straight quarter of negative growth.

And that was only up to Thursday!

And what did the financial markets do with all of this?

They rallied HARD.

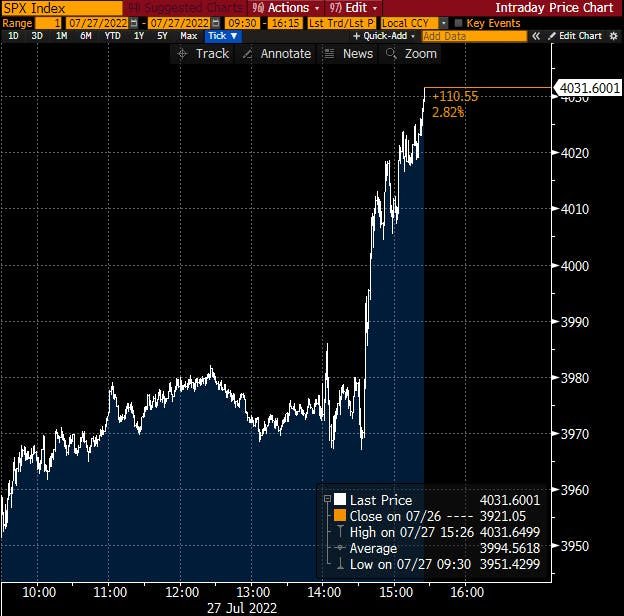

The S&P 500 ended the week up 4.3%. The tech-heavy NASDAQ did even better at 4.7% from Monday to Friday.

In fact, in July, we just had the best month for the S&P 500 since November of 2020 and the double events of Covid-19 vaccines and a new presidential administration. All in all, quite a feat.

Why?!?!

Well, the key is likely the US central bank's outlook and, in particular, the sentence with which we began this week's newsletter. To save you scrolling back up, Chair Jay Powell said:

"We are now at levels broadly in line with our estimates of neutral interest rates, and after front-loading our hiking cycle until now we will be much more data dependent going forward’.’

The head of the US Federal Reserve is saying that, going forward, they will base their decisions far more on the upcoming economic data rather than their previous concerns that they were behind the curve in dealing with inflation.

In other words, the central bank recognizes that growth is slowing sharply and they must be both open minded and careful about dogmatically tightening policy and raising rates further.

You can see how investors liked what they heard during Chair Powell's press conference that began at 2pm:

If it seems puzzling to you that the markets LOVED the idea that the central bank is acknowledging that the economy is slowing, then you would not be alone.

But perhaps the best way to think about it is that the Fed is saying: we hear your concerns about the hard landing and are ready to be flexible in our approach going forward.

i.e.: we might not crash the economy into a cliff after all.

On the recession point, there has been A LOT of attention given to whether the US is entering a recession or not.

Most of it is obviously politically motivated and pretty banal. We don't feel like it matters overly that the economy has shrunk the last two quarters. It was obviously running very hot and now, thanks to monetary policy has now cooled substantially.

As we have stated before:

Growth is slowing and, in fact, it must moderate in order to get inflation under control.

But the employment situation is exceptionally strong. And it isn't the only data point either: plentiful job openings, rising wages, and people partying like, well, they haven't done so since 2020.

And yes, before we hear about it in our mailbox, it is likely that the employment situation will weaken in the months ahead. That is another - exceptionally unfortunate - inevitable part of our campaign to slow rising price pressures.

And it is equally correct that employment is a lagging indicator that moves after the business cycle has weakened. All true.

But, typically, in most recessions employment is not historically robust as it is now. In fact, it would already be weakening quite sharply by now. After all, GDP is another lagging indicator. We are talking about the GDP growth for January through the end of June.

Anyway, as we said above: All of this is pretty boring and a lot of it is politically motivated which is perhaps understandable but also lame. There are plenty of very serious problems at present - economic or otherwise - we don't need to go around inventing new ones.

The important takeaway from both Chair Jay Powell's remarks AND the GDP print is something avid readers of this newsletters already knew: the recovery is over.

And so why then, did equity markets take off after these twin-events?

Two large reasons:

As we detailed in our introductory note and go into greater depth below, because investors were overly bearish. A lot of bad news was "priced in" to the markets.

Second, and far more uncomfortably, because the Federal Reserve signaled an end to the tightening of monetary policy. The assumption is that more moderate growth is leading to more moderate Federal Reserve monetary policy thereby preserving the possibility of a soft economic landing and, if it isn't, a wave of liquidity in the form of more quantitative easing (and interest rate cuts) may be in the offing.

The best evidence for this is that many of the largest technology companies produced disappointing earnings this week and yet the stocks rallied (see below).

Stocks that do well in low growth, easy monetary policy periods did very well this past week.

And that is why we remain very concerned. The chance of an easing in monetary policy is still very remote.

Inflation is still over 9%!! It may begin to moderate - there is that word again - but that doesn't mean it is low or that our problems are behind us.

There is no guarantee that a recession isn't in the offing or that more and faster interest rate rises are not possible.

We may end up being exceptionally wrong. We would love to be but it seems pretty unlikely to make that call right now.

More positively, we can't be wrong about inflation having peaked AND the above. It can only be one or the other!

*******

Have questions? Care to find out more? Feel free to reach out at contact@pebble.finance or join our Slack community to meet more like-minded individuals and see what we are talking about today. All are welcome.