Could The S&P 500 Reach The 5000 Level? Why Could It Happen And When?

One recent trend is that analysts and investors have been increasing their target forecasts for the S&P 500 (and other major US benchmarks) in the new year.

This is perhaps to be expected. As the "soft landing" thesis for the US economy has become the default scenario, optimism has grown about 2024 and what the future could hold.

One of the (big) numbers that is being thrown around is 5000.

As in, the S&P 500 could rise to 5000.

That wouldn't just be an all time record high, it would obviously also be a big psychological number with all sorts of banner headlines on newspapers/social media/TV/you name it.

Big round numbers are irrelevant in many respects but they also capture imaginations and drive narratives and, as this newsletter has constantly argued, narratives can be very powerful force when it comes to framing and determining events. ChatGPT and its competitors do not make a lot of money but their great magic trick is to use technological convinces people they inevitably will.

Furthermore, the S&P 500 to 5000 may seem like a big jump but in fact it is only around ~10% from the S&P 500 current level of 4590.

Pretty amazing what can happen even when you are paying attention. Quietly and quite quickly, the S&P 500 has risen nearly 800 points from its low earlier this year. That has been a 20%+ move but it also means that the index of large companies is nearly back at the record level reached back when interest rates were at a record low!

There are two reasons people are broadly calling for the market to head higher still in 2024:

Interest rate volatility is down

Many investors need to chase returns.

On the first point, this is a bit esoteric but, because there is greater certainty about what the Federal Reserve will do going forward, there is subsequently less volatility of people jumping into and out of positions and assets based on the latest data point.

On the second, a lot of professional investors are under-performing their target benchmarks and are therefore buying - with leverage! - and racing to catch up with the overall market.

This might work if done as an individual but in aggregate it has the response of.....sending the market higher!

The key question, however, might be less about whether US stocks head higher from here. Instead it might be: if stocks continue to rise what parts of the market will do so? And why?

By that we mean: what sectors and types of companies will outperform others and the also the broader index?

The story isn't just important for what could provide better returns - always nice! - but also because it will help give you a simple roadmap for monitoring whether this thesis has a way to run (5250! 5500!! Higher still!) or not.

One of the most interesting aspects of the last few weeks is that it hasn't been the biggest companies that have been doing the best.

The S&P 500 companies have done fine but the real outperformers since the October meeting of the Federal Reserve are small cap US companies.

By "small cap" we mean small capitalization. i.e.: smaller publicly traded companies.

See here comparing the S&P 500 - an index of the largest publicly traded US companies - with the Russell 2000 index of small cap US companies since the Fed's "pause" meeting in October:

This isn't getting a lot of press because at the time of writing the S&P 500 and Nasdaq are only around 2-4% from their all time highs.

Meanwhile, the Russell 2000 index of small cap companies has fallen over 24% from its record highs and is only up around 6% for the year at the present time.

That might be changing now for one simple reason:

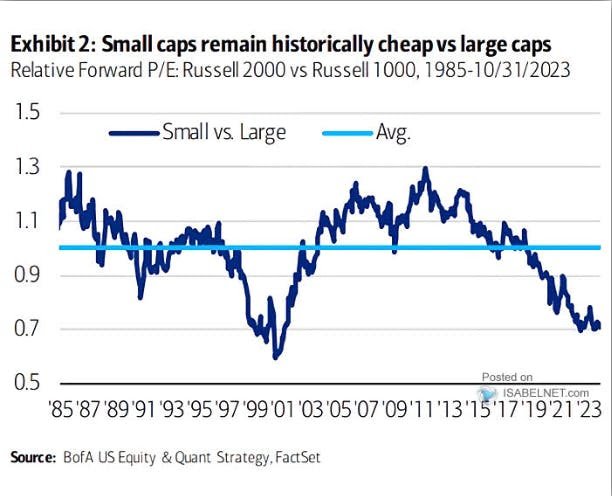

US small cap companies are cheap.

These companies' shares have a far lower valuation on an absolute basis.

But they are also extremely cheap vs the S&P 500 and even more so against the most frothy Super 7 stocks that gain from the AI mania.

See here:

It isn't just the relative valuation though it is also the expectation that they will do very well in the current environment.

The logic driving that thinking is that small companies - unlike their larger brethren - rely on financing for a lot of their investment. Like most of us, small companies simply struggle to make enough capital for their needs and so they must borrow at market rates to invest and grow.

When rates are high and heading higher this reality is very expensive and furthermore, it means that small cap companies surrender a lot of their profit to higher interest rate costs.

This has the knock on effect of making their stocks less attractive to investors.

If given a choice between large companies that are less negatively affected by high rates and small companies that are, investors unsurprisingly chose the former. They would rather own a company like Apple that is largely unaffected by higher interest rates than own a small Apple supplier that must borrow to build a new plant or product.

What could change the relative attractiveness of small cap companies?

Economic weakness.

If the economy suddenly starts to weaken for any reason. If defaults rise and companies struggle to cover their debts then small companies will also underperform.

That is why we are typically so cautious about recommending small cap stocks. While small companies are very wonderful (look at us!) the window where they do better than larger companies is very, very small .They struggle if interest rates rise and struggle if the economy turns and interest rates are cut in the expectation of a recession.

Things have to be juuuuuust right for them to do well and we might be in a period where that can happen right now.

How long will it last?

Great question.

It could go for some time as long as the present benign economic and moderating inflations conditions continue.

So, for now, rather than rush out to load up on smaller US stocks the smart thing to do might be simply to watch how they do. You can easily track a broad based index like the Russell 2000 or even an ETF that tracks the index like IWM on your smartphone and watch carefully for them to start to weaken - both relative to the S&P 500 and on an absolute basis.

Doing so both on their own and relative versus the S&P 500 will be a great way to quickly and easily monitor just how confident investors are about the direction of the economy and, in turn, interest rates.

Small cap companies aren't the only part of the economy experiencing better conditions either....

*******

Have questions? Care to find out more? Feel free to Download our App (!!) or reach out at contact@pebble.finance or join our Slack community to meet more like-minded individuals and see what we are talking about today. All are welcome.