2023 Theme - The Big Companies Getting Bigger

As the financial markets and millions of American depositors tried to digest the collapse and sale of First Republic Bank the Federal Reserve released their report on Silicon Valley Bank's collapse way back in March.

Among other things, the post mortem is pretty critical of the Federal Reserve's regulatory performance. That is very welcome but it also argues that the solution to those failures is a stronger Fed supervisory arm and extending "enhanced prudential standards" to mid sized banks.

So, we are in effect going to raise the regulatory burden on regional banks but also bracket them in the "too-big-to-fail" bucket along with the likes of JP Morgan, Citibank and Bank of America.

This will mean that both the costs of banking services and the moral hazard of being too big to fail will both increase.

Or, put differently: costs up, risks up.

Got it.

A few top level takeaways:

One way of looking at this document is that every time there is a failure of regulation the answer is ALWAYS and without fail, more regulation. Funny how that always seems to be the case.

A second way of looking at this document and the prescriptions therein is that it is a recipe for a far larger and more sclerotic US banking system.

And, as we have argued before, that is really what we really think the outcome will be here:

More banking regulation and a more concentrated banking sector. We are very uncertain that this will be either better for the US economy or "safer" for financial stability.

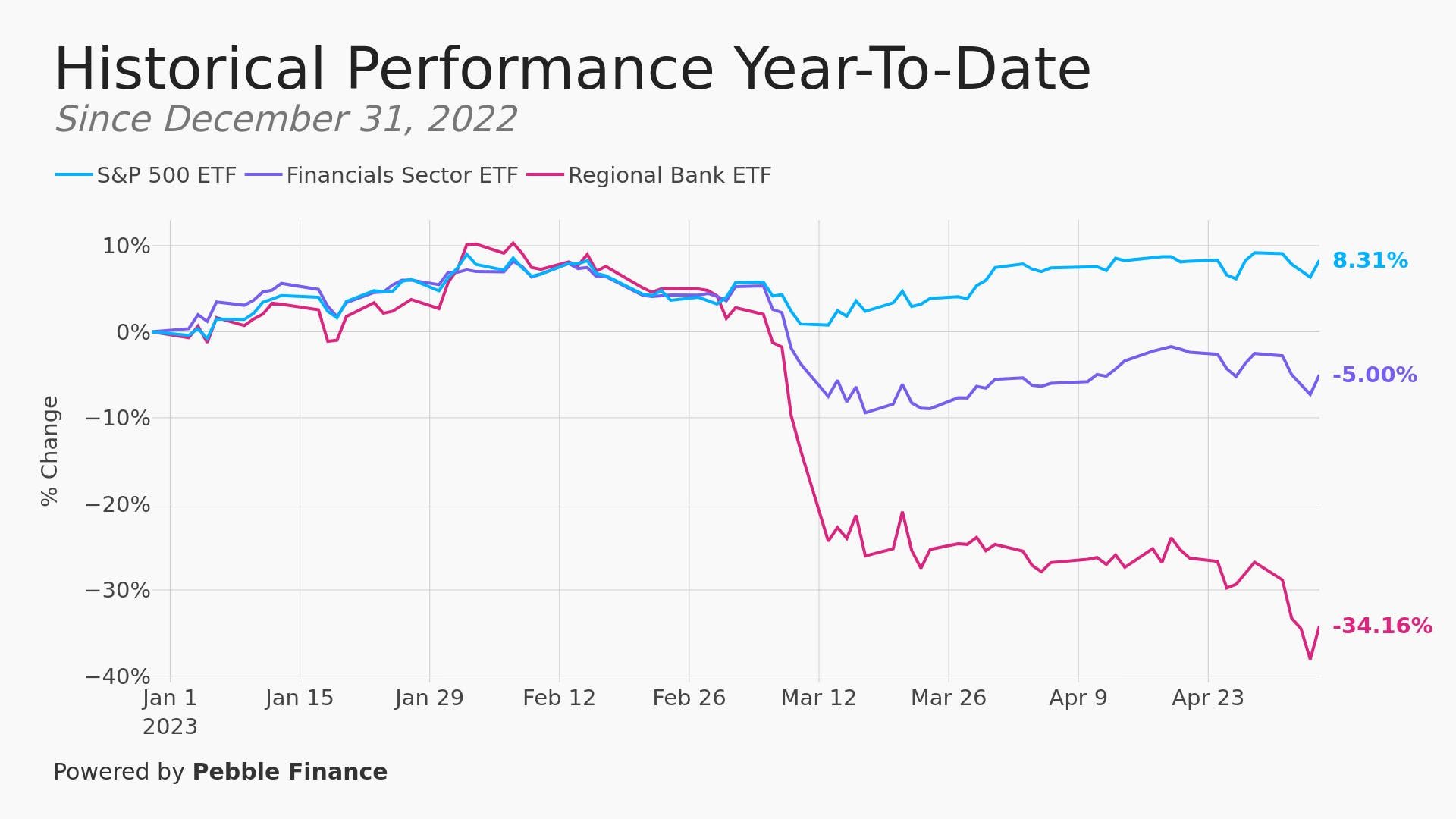

Here is what that looks like in practice:

The main S&P 500 financials sector is doing reasonably fine while the regional bank ETF has fallen off a cliff.

This will have consequences: it will tighten US financial conditions in the short term but the most important development might be over the long term changes it has within the US banking system.

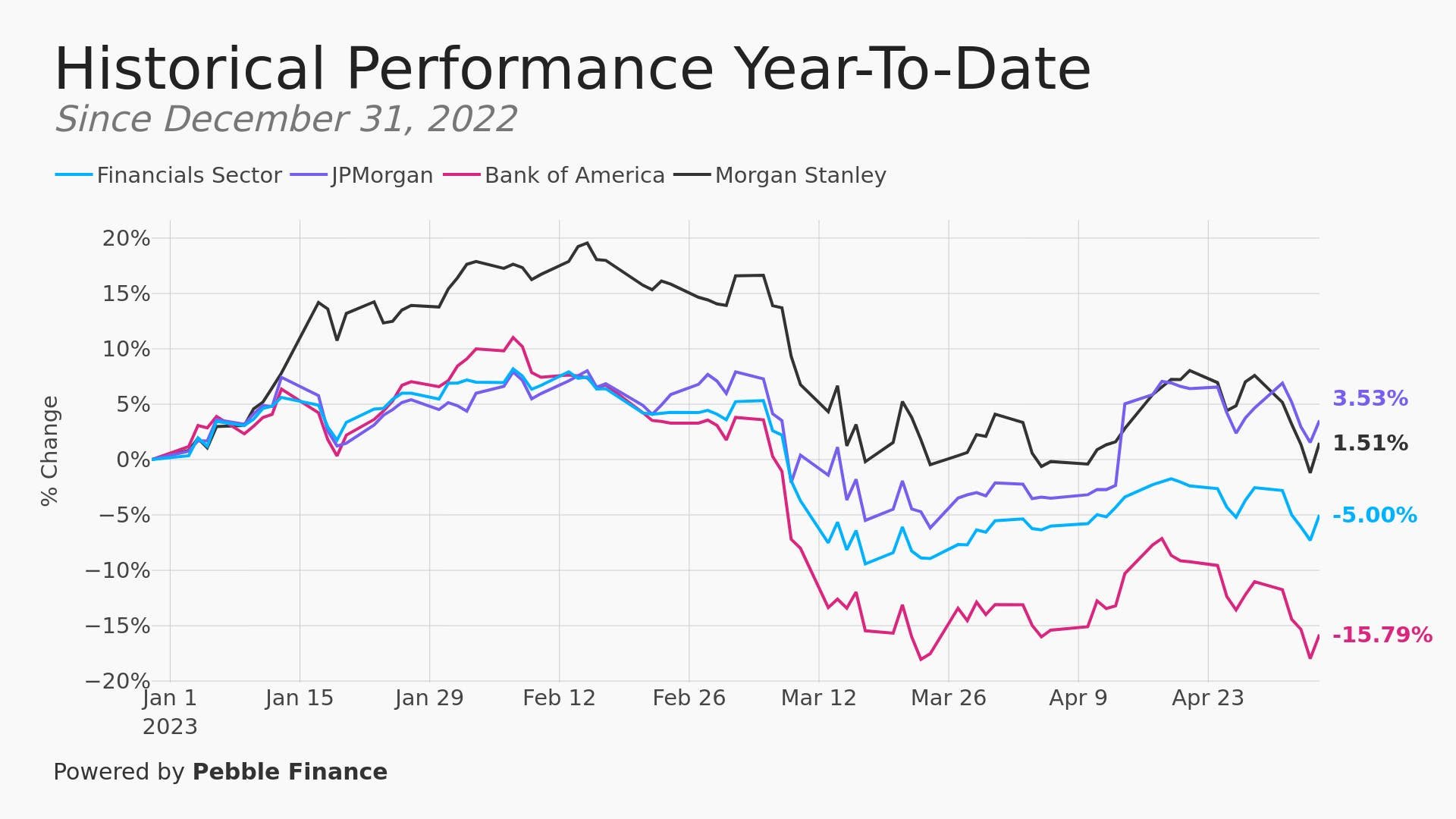

Here you can see how some of the largest "SIFI" or Systemically Important Financial Institutions" are doing:

One takeaway from rising share prices over the medium term is that the big are getting bigger. That is good for them and their shareholders, it is largely bad for the rest of us, no matter who you are. If you don't believe us we suggest you try and get a mortgage from any of the big 5 US lenders some time. Take 16 aspirin and prepare for a long haul.

It is pretty ironic that the Democratic party has become the party of "big" but even more incredible the party of "Big Banks." They would strongly disagree, of course, but the proof is in the outperforming JP Morgan share price above.

There is good reason for that. By one calculation JP Morgan has received a discount of $18 billion on $168 billion of First Republic assets. That is worth $500 million annually, in return for a $10 billion cash payment.

Nice work if you can get it....

That push towards larger and more sclerotic might be politically tenable - just - but not if the institutions charged with the critical job bank regulation keep making a major hash of it.

Credit to Michael Barr and the others at the Fed who put together the report that they are critical of their own regulatory performance in this report. However, in time honored bureaucratic fashion they mostly blame their predecessor and one-off mistakes such as not being willing to quickly downgrade the bank in 2022 after it had been rated "Satisfactory" by the previous regime.

When the new team observed weaknesses in governance and risk management late in 2021, they were reluctant to issue a downgrade within seven months of the issuance of the prior rating without doing more examination work to support a change in view and related action.

In other words:

"The bank was bad from a risk management standpoint and we knew it but we didn't want to upset anyone."

Not terribly inspiring when the desired outcome from this report is MORE regulatory power for this institution.

The real issue however, is the fact that the report treats the SVB issue as a one-off when as events have demonstrated, it very much isn't.

Rather, it is glaring how the overall regulatory framework has missed a very obvious and ongoing structural issue with the US banking system. The report is several hundred pages long so we may have missed it but there wasn't any real discussion of the fact that SVB and, indeed, all banks are directly incentivized and in fact told to buy certain types of highly liquid and super safe assets to protect against default.

There are two problems with this issue:

The first is that there has been a lot hay made from the Trump era bank reform that made it easier for regional banks like SVB to take more risk and hold less very liquid assets.

The only problem is that, as the Federal Reserve report does allow, SVB was very, very close to matching the levels and could have done so with a bit of effort. No, the real problem was something we have already discussed:

Silicon Valley Bank had plenty of assets but they had to sell these assets at a loss. That loss rather than how many assets they owned, was the spark that lit the fuse that quickly led to their bank run.

This brings us to the second point. The losses occurred because these very liquid assets (namely US Treasury bonds and assets issued by US sponsored entities such as Fannie Mae and Freddie Mac mortgage bonds) have lost significant amounts of value as the Federal Reserve has embarked on the fastest interest rate hiking cycle of all time.

This oversight was striking, as we say above, not least because it would be the most obvious outcome from the very actions of the Federal Reserve itself.

We made mention of this last month when we pointed out that the Federal Reserve's periodic regulatory "stress tests" of bank balance sheets had no scenario of rapidly rising interest rates. As if interest rates would simply never, ever rise quickly.

Put a bit more structurally, one part of the Fed was unprepared for a scenario that was unleashed by a course of action embarked upon by another part of the Fed.

So, not some impossible Black Swan event like an alien invasion or World War III or a pandemic unleashed by a zoonotic virus but rather just a bog standard interest rate cycle made necessary by run away inflation.

Two last thoughts that concern us:

The first is simply a question about whether we will get a similar report about every single regional bank that is experiencing serious issues (or has to be wound down and sold)?

The second is whether the Biden administration and its allies in Congress understand the gravity of a slow rolling bank crisis that gradually picks off bank after bank around the country?

A single or even a few banks going down because of regulatory lapses and a "textbook case of mismanagement" by bank leadership as Michael Barr argued but these are adding up to be quite a bit more than a one off.

Going forward, the question for the US banking system becomes not:

How long can you keep arguing that "our banking system is sound and resilient" as official after official keep repeating.

But rather:

What to do about a far bigger issue of a self inflicted recession caused by a Federal Reserve that a) let inflation get out of hand and b) then was forced to raise interest rates and didn't account for the danger that these actions posed to the banking system, that they are also in charge of?

This newsletter has carefully avoided trying to write about "damaged Fed credibility" or the more crackpot arguments against the Federal Reserve system because we don't find these points very actionable and often feel like you end up looking, well, sort of unhinged.

But if an economic recession is created through a combination of lack of action and lack of oversight on two of the three main criteria (inflation and financial stability) by the most important and independent American financial institution then it will look very bad.

At the very least the case will be made for a serious overhaul of the institution by its political overseers and in a day and age where both major parties alternate between acting stupidly and acting foolishly, that is a very worrying thought.

Change doesn't have to be bad but in an era of political volatility and the Great Forgetting it would make us very nervous.

*******

Have questions? Care to find out more? Feel free to reach out at contact@pebble.finance or join our Slack community to meet more like-minded individuals and see what we are talking about today. All are welcome.