2022 Theme: The Big One - How Goes The Effort To Combat Inflation?

It's that time of the month again....

The US inflation number was published and everyone over reacted and over extrapolated and over many-other-things besides from a single data point.

Now it is our turn!

The difference is that this month the surprise was in the other direction and, most importantly, the details were also very solidly in favor of the lower inflation thesis.

This was very welcome and not just for humble (and somewhat nervous) financial scribblers who have suggested this was likely for the last few months.....

As you may have noticed 5 of the last 6 US inflation numbers have come in very high AND also far above the average expectations. That was a nasty double whammy that, unsurprisingly, caused the market to sell off each one of those 5 occasions.

Well, the very opposite happened this time around.

Here are the basics:

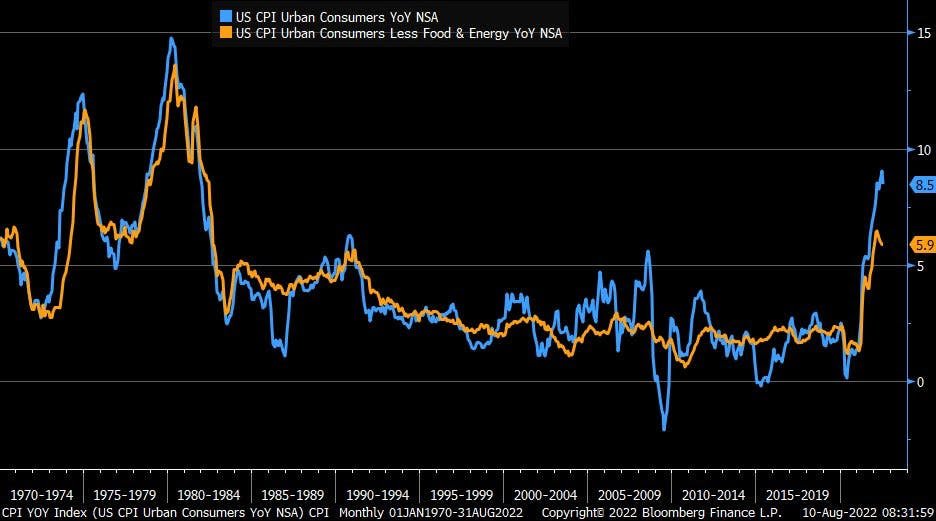

The consumer price index rose 8.5% in July from a year ago, below expectations. In one sentence: this was due largely to slumping energy prices (see below).

Excluding volatile food and energy prices, so-called "core CPI" rose 5.9% annually and 0.3% monthly, compared with the estimates of 6.1% and 0.5% respectively.

The report was also good news for workers beyond just falling prices. They also saw a 0.5% monthly increase in real (i.e.: above inflation) wages.

All of this was obviously great.

And here are the takeaways.

There are three related to:

Market timing.

Inflation is still really high.

Be very careful.

The big one is:

We are now at 4 straight months of Core (which excludes volatile items like energy and food) CPI inflation decline! Hilariously this didn't matter when we quietly pointed it out after the last two CPI prints. However, this time, all of a sudden, wham.

As ever, market timing is tough! Here is the relevant chart:

The second takeaway is the very basic point that this was a big drop and very welcome! But a 0.3% monthly increase in core CPI is still very large on an annual basis. Add it all up and it comes out to 3.75% annualized.

For context, that is almost double the Federal Reserve's target of 2%, and higher than ANY point reached during the last hiking cycle.

So, higher interest rates from here are a near certainty.

Because inflation is still at elevated levels, the Federal Reserve not only should do more but rather, it must do more. At some point in the future the central bank will suddenly recognize just how much more work they must do.

The final takeaway is: be cautious.

We haven't been surprised by the bounce. One was overdue in June but we have been pretty shocked by both the strength and length of the rally, especially considering the available data. As always, markets can overreact in both directions!

But the overall market narrative has been remarkable. We have flipped, in the last 6 weeks, from believing a deep recession was a near guarantee to now believing it is extremely unlikely. In other words, we have flipped - mid tightening cycle! - from a hard to a soft landing all in a matter of weeks.

Quite the move.

The core reason for this shift is the continued - and impressive - strength and resiliency of the US economy. That is a wonderful thing and long may it last but just be aware that this narrative is just that, a narrative.

And none of this decline is set in stone. Or even mud adobe! It could easily flip back.

Here is one specific note of caution from the CPI report itself: the vast majority of this month's lower inflation is directly derived from lower energy prices.

You can see that very clearly here:

That is very wonderful but it is also very easily reversed: what can go down, can still go up. And perhaps no sector is as easily influenced as energy, which is exceptionally volatile (hence why it is excluded from the "Core" part of CPI).

And, as we have detailed, there are a few concerning factors about the price of energy right now.

As Europe learned to its cost last autumn, in a world rapidly transitioning to a greater renewable energy mix, we are increasingly dependent on the wind blowing (or sun shining), as oil pumping or gas flowing.

You do not have to look very far to become very concerned about, not just the war in Ukraine and Russia's oil exports, but also the broader energy market. There is still very little supply and a lot of demand.

For now, as regular readers know, we have written before about how, for central banks, the oil price is absolutely critical. It not-so-quietly determines so much.

In an earlier edition of this newsletter, we noted:

In other words - exogenous shock or not - the Fed will create conditions to curb oil demand sufficiently to lower its price significantly.

And oil and energy costs have come down the last two months. But if they rise, for any reason, intended or not, then so will inflation.

A lot continues to hang on the oil (or gas) price and the overall energy complex.

We will turn to these topics in the weeks to come but now we turn to the second rather impressively good piece of news to emerge this week.

*******

Have questions? Care to find out more? Feel free to reach out at contact@pebble.finance or join our Slack community to meet more like-minded individuals and see what we are talking about today. All are welcome.